It can feel like the guidance on climate mitigation is constantly changing, like the goalposts are moving, and it’s hard to keep up. The good news is that the foundational principles are relatively simple. Bring capital to the highest-impact solutions you can. Size your capital investments based on the scale of both your emissions and your profits. And take immediate action.

When it comes to sizing your climate investments, guidance recommends establishing an internal carbon fee. But how, why, and to what end? The use case and mechanisms for applying an internal carbon price or fee have evolved over the last two decades. In this article, we trace this evolution and share recommendations and resources to help company representatives understand the changing landscape and consider how a carbon price might support their climate action strategies.

What is an internal carbon fee?

An internal carbon fee applies a price to every tonne of greenhouse gasses emitted by a company in order to incentivize low-carbon business decisions. In some cases, this was an actual fee levied on each tonne of emissions, which would go towards a decarbonization budget. In other cases, it was a “shadow price,” used to tip the scale towards investments with low-carbon performance.

Evolving methods for calculating an internal carbon fee

The practice of organizations setting an internal price on carbon began to gain steam in the early 2010s. Early on, internal carbon prices were generally set based on a cost of abatement (e.g. the company’s estimated cost of reducing its own emissions), the social cost of carbon (e.g. the cost of the damage of climate change to society), or an estimated potential regulatory carbon price.

In 2010, the Obama administration established the first social cost of carbon for the U.S. at $43/tonne. In 2013, 29 companies, including Disney, Exxon, Google, and Microsoft, disclosed to the CDP that they were using an internal carbon price in their decision-making. That year, Microsoft also published guidance for establishing an internal carbon fee.

At COP 2016, a new High-Level Commission on Carbon Prices was created to guide the design of carbon pricing instruments. By 2020, close to half of the world’s 500 largest companies had either established an internal carbon price or were planning to do so in the next two years, according to a CDP report. The top reasons cited included driving internal behavior towards reductions, investing in low-carbon and energy efficiency projects, stress-testing investments, and navigating the regulatory landscape.

Across this period, the conversation around the internal carbon fee mainly highlighted its purpose as a tool for incentivizing internal reductions within organizational value chains. The theory was that a price would help companies visualize, track, and make business decisions based on emissions, while in some cases creating a budget for investment in internal decarbonization initiatives.

SBTi, WWF and GoldStandard Guidance

Alongside the evolving landscape of internal carbon pricing, in 2015, the Science-based Targets Initiative was founded to provide guidance to support companies in setting internal reduction targets in line with a 1.5 or 2℃ warming scenario. Over eight years, with over 3,300 validated company targets established, SBTi has become the go-to climate framework for the largest companies. The Initiative continues to develop rules about what types of action “count” toward a target and how they should be accounted for. Their guidance seeks to incentivize internal reductions; the framework does not recognize or incentivize investments in climate action projects outside of the direct value chain.

In 2020, WWF published the Corporate Climate Mitigation Blueprint. The guidance’s intent was to expand corporate ambition beyond value chain boundaries toward longer time horizons, systemic change, and scaled finance. A collective approach is necessary, it argues, “to achieve the kind of scale that science tells us is needed to achieve system transitions in land and ecosystems, energy, urban and infrastructure, and industrial systems.”

The Blueprint guides companies through a four-step model for a holistic climate action strategy. The first steps are for companies to 1) measure and disclose their emissions and 2) reduce value chain emissions in line with a science-based target. Then, it guides companies to 3) create a climate contribution budget that internalizes the cost of any remaining emissions, and 4) use that budget to invest in high-impact climate and nature actions. Companies are encouraged to disclose the “implicit carbon price” associated with that climate contribution budget. Here is the introduction of a new paradigm for the use of carbon pricing focused on collective support for climate projects beyond a single company’s value chain. Rather than incentivizing internal reductions (which, under this framing, should be happening already), this new version of a carbon fee provides support for collective global decarbonization efforts – whether through investing in R&D, high-quality carbon projects, or other mechanisms.

In May of 2023, Gold Standard published its own new guidance for a comprehensive corporate climate strategy, titled “Fairly Contributing to Net Zero.” The guidance, aligned with the WWF Blueprint, encourages companies to, alongside meeting science-based reductions, “take responsibility for ongoing emissions by setting an internal carbon price and funding climate action beyond the value chain.”

How to prioritize internal and external initiatives

At Native, we are aligned with both the WWF Blueprint and Gold Standard Guidance in their recommendations that companies set and make plans to meet rigorous reduction goals while also supporting collective action – now and into the future – beyond their value chains. Foremost, this guidance encourages a bias towards action now. Secondly, if climate finance is part of a company’s climate strategy, the method of establishing a transparent internal fee to create a contribution budget eliminates the financial pressure to support low cost, and potentially lower-impact projects. It steers companies towards focusing on “collective contribution” rather than “carbon neutrality,” which we see as a more credible and appropriate strategy for employing and claiming carbon project investment.

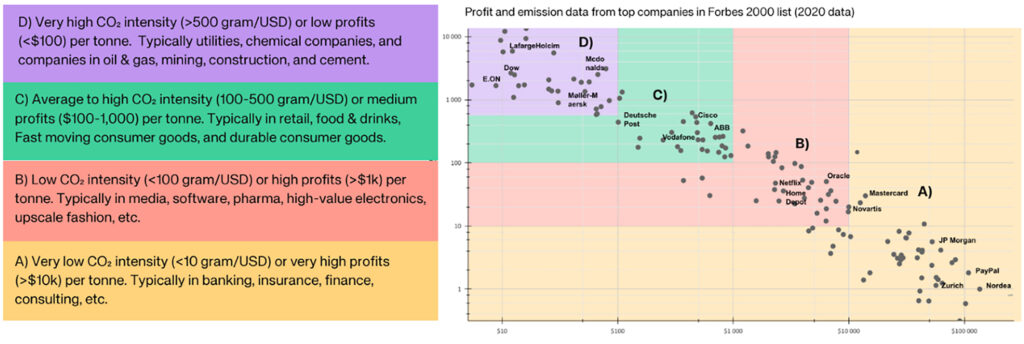

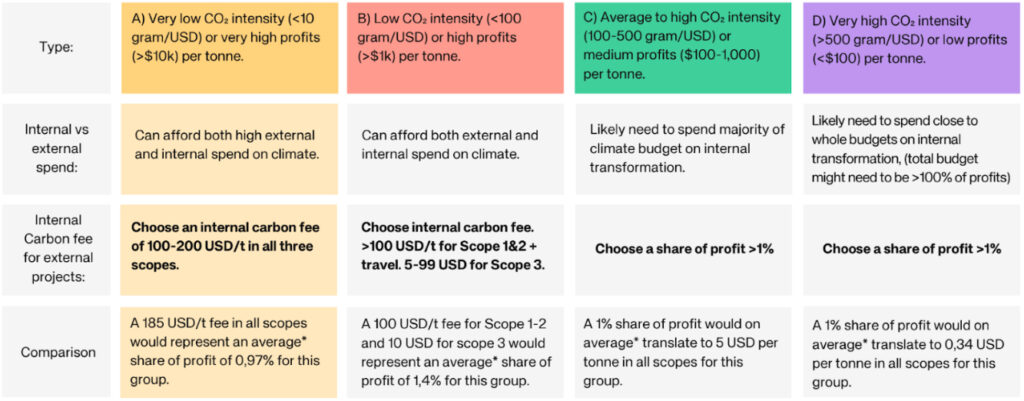

But not all companies have the budgets and resources to both meet an internal reduction target and create a climate contribution budget at a credibly high carbon price. The Carbon Gap “Bridging the Ambition Gap” Report and Milkywire’s white paper on setting an internal carbon fee speak to this issue. Both argue that a company’s carbon fee for investment in external projects should be determined based on its “profit per tonne” (e.g. its total profits divided by its total emissions) and its ability to use money to finance its own emission reductions. The Milkywire report breaks down four categories of industry types based on how different operating and production models create earnings and emissions. In the A category, non-material companies in the finance, banking, insurance, and consulting sectors have the highest profits per tonne emitted, often over $10,000 per tonne; at the same time, they have limited opportunities for internal reductions. In contrast, companies in the D category – utilities, chemicals, construction – are likely to have profits below $100 per tonne with massive opportunities for internal decarbonization. Thus, the paper argues that companies in category A should set a high carbon fee to support external projects and invest internally where possible, while companies in category D should focus on investing heavily in internal decarbonization efforts and commit a small percentage of revenue to external projects rather than establishing a carbon fee.

When looking at these different resources, a number of questions arise: How should a company apply its specific context to setting an internal carbon price? What should be the order of operations? And should a company set two carbon prices: one for internal reductions and one for external climate investments?

An internal carbon price within a holistic climate strategy

Here’s our current thinking on what could make sense as a general pathway for thoughtfully applying a carbon price (which is sure to have credible caveats and alternatives). All companies across industries could look to set an internal carbon price to establish a climate investment budget – based at or above their cost of abatement, established research on the social cost of carbon, or another credible mechanism that takes into account their profit/tonne – and communicate it transparently. Having done that, a company could look to deploy that capital towards decarbonization to reach or exceed its internal reduction targets. Any capital from that budget that is not invested directly into decarbonization could be invested in beyond value chain high-impact climate work, whether that be in R&D for new climate technologies, early-stage investment for new high-impact climate projects, or another rigorous climate investment mechanism. Though there may be circumstances where there is a good case for holding a budget across years in order to make a necessary large-scale investment, we believe that in most cases companies should design in some form of pressure to invest the climate budget in the given year (or as early as possible) to favor the immediate climate action we need.

Most importantly, we recommend that companies keep in mind the foundational principles: Bring capital to the highest-impact solutions you can. Size your capital investments based on the scale of both your emissions and your profits. And take immediate action.

Resources:

How-To Guide to Internal Carbon Pricing (Ecofys, Generation Foundation)

Fairly Contributing to Net Zero (Gold Standard)

A Guide to Climate Contributions (New Climate)

A Contribution Approach to Climate Finance (Native-hosted webinar)